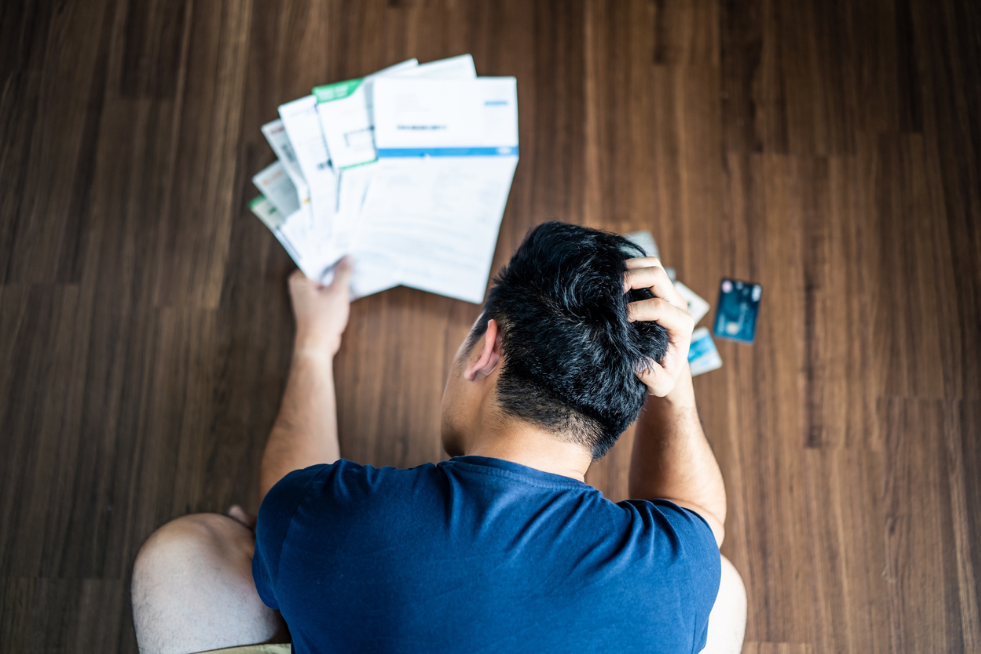

For many of us, the number of different places we borrow from can stack up over time. A credit card for everyday spending. Car finance to help pay for the car you use. Perhaps a small personal loan taken out for a specific purpose. Individually, these repayments may feel manageable but, together, they can make budgeting more complicated than it needs to be.

Often, it’s not the total balance that creates pressure, it’s the admin: different due dates, different interest rates, and different minimum payments to track.

That’s where debt consolidation can start to look appealing. Not as a way to make debt disappear, but as a way to simplify how it’s managed, and potentially even reducing the cost of managing it.

Here’s what to consider before deciding.

Debt consolidation usually involves taking out one new loan to repay several existing debts. Instead of juggling multiple repayments, you combine them into a single monthly payment.

Ideally, the new loan has a lower interest rate than the debts it replaces, or at least a fixed repayment term so you know when you’ll be finished.

For example, imagine you owe £4,000 across two credit cards. If you’re only making minimum payments at high interest rates, a large part of what you pay each month goes towards interest rather than reducing the balance. That can make it feel as though the debt isn’t shrinking very quickly, especially if you’re working long shifts as a nurse, teacher or police officer and don’t have hours spare to keep reviewing your finances.

If you replaced that £4,000 with a loan at a lower interest over a fixed term of say three years, you would have one set monthly payment and a clear end date. You’d know exactly when the debt would be cleared and how much you’d repay overall.

There are alternatives to debt consolidation loans that are also worth exploring. For example, you could consider a 0% balance transfer credit card instead, although fees typically apply and the rate tends to increase after the promotional period.

Consolidation tends to work best when it genuinely improves your position.

It may be worth reviewing if:

For someone working long or irregular hours, moving to one fixed repayment can reduce the risk of missed payments and make monthly planning simpler. The value isn’t just financial, it’s practical.

It’s worth remembering that while debt consolidation can help, a lower interest rate is not guaranteed. Lenders will assess your credit history and affordability before deciding whether to offer a loan and at what rate, so it’s important to check that the overall figures work in your favour.

Consolidation can cost more if it simply stretches repayments over a longer period. A lower monthly figure can feel like progress, but if you’re paying interest for longer, the total cost may increase.

You should also check if your existing debts have any early repayment charges associated with them. If so, even if you end up getting a lower interest rate on the debt consolidation loan, the amount you’d have to pay to clear the original debt early might offset any savings you make on the interest rate.

Bear in mind that closing credit cards after debt consolidation can sometimes affect your credit score, particularly if it reduces your available credit or shortens your credit history.

It’s also important to avoid clearing balances only to rebuild them. If new borrowing builds up alongside the debt consolidation loan, you’re back where you started, just with a different structure.

Some debt consolidation loans are secured against your home. Using one to repay unsecured debts increases the level of risk, as missed repayments could ultimately put your property at risk.

Before making any changes, take a clear look at your current situation.

Even a small difference in interest rate can make a meaningful difference over time depending on your loan amount and repayment term. And for some people, having one clear repayment plan can make it easier to stay on track.

If debt consolidation looks like it could help, the next step is to compare what’s on offer. Look beyond the headline monthly payment and check the total repayment cost and term.

Checking eligibility first can also reduce the likelihood of unnecessary hard credit searches affecting your score.

Blue Light Card members can use our partner Clearscore to compare what loans they might be eligible for in one place. Additionally, for a limited time period until 15 March, Blue Light Card members will also receive a £30 Amazon voucher when they take out a loan via Clearscore. If you do take out a loan via Clearscore, Blue Light Card may receive a commission at no extra cost to you. Representative 17.7% APR variable.

Blue Light Card Ltd is an Introducer Appointed Representative of ClearScore, who are authorised and regulated by the Financial Conduct Authority. Blue Light Card Ltd will receive a commission from ClearScore if you take out a product through ClearScore. ClearScore is a credit broker not a lender.

*If you’re struggling with debt, free and confidential advice is available from Money Helper at www.moneyhelper.org.uk

It can help you understand all your options before taking out further credit"

Does debt consolidation save money?

It can, particularly if the new loan has a lower interest rate or shorter repayment term and you don’ t have any early repayment charges on your existing debt. However, it’s not guaranteed so always check the total cost of your debts over time in order to compare.

Is debt consolidation bad for your credit score?

Applying for credit can cause a temporary dip as most lenders require a hard credit search on your credit file. However, if it helps you stay on top of repayments better than you were doing before, it could help you improve your score over time although this is not guaranteed.

Is it better to consolidate or pay off debts separately?

It depends on interest rates, early repayment charges, repayment terms and whether consolidation genuinely improves your overall position.